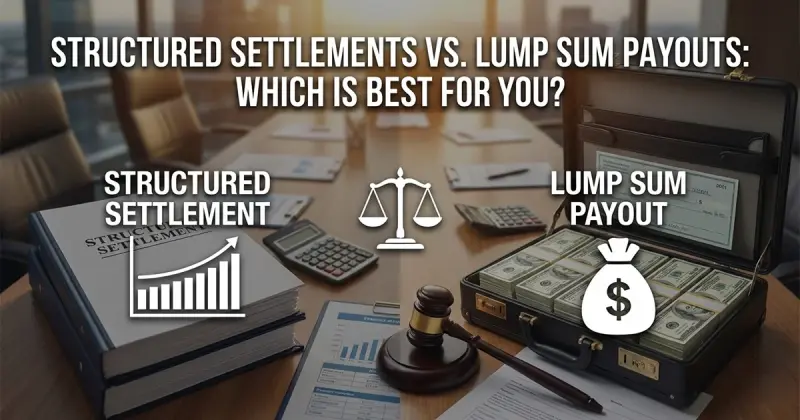

Deciding between a structured settlement and a lump sum? We break down the pros, cons, and tax benefits to help injury victims make the right financial choice.

Imagine you’ve just won a major victory. After a long legal battle regarding a personal injury, the court or insurance company agrees to pay you a significant amount of money. Finally, the stress is over! But wait—now you have to make one of the biggest financial decisions of your life.

They ask you: "Do you want all the money now in one big check, or do you want monthly payments for the rest of your life?"

This is the battle between Structured Settlements and Lump Sum Payouts. It sounds like a good problem to have, but picking the wrong option can cost you thousands of dollars in taxes or leave you broke a few years down the line.

In this guide, we will break down exactly what these terms mean, compare them side-by-side, and help you decide which path leads to the best financial future. Plus, we have selected top expert attorneys from Best Attorney USA who can help guide you through these complex legal waters.

What is a Lump Sum Payout?

A Lump Sum Payout is exactly what it sounds like. You get the entire amount of your settlement money in one single payment.

Think of it like winning the lottery and choosing the "cash option." If you settled for $500,000, you get a check for $500,000 (minus lawyer fees and expenses) deposited into your bank account immediately.

Why Choose a Lump Sum?

The biggest advantage is freedom. You have total control over your money from Day 1.

-

Pay off debt: You can instantly pay off high-interest credit cards, student loans, or your mortgage.

-

Big purchases: You can buy a house or a reliable car to get to work.

-

Invest: If you are good with money, you can invest it in the stock market or real estate and potentially make it grow faster than a structured plan would.

The Downside of Lump Sums

The biggest risk is you. Many people aren't used to managing large amounts of cash. Statistics show that many people who receive large windfalls spend it all within a few years. Once the money is gone, it’s gone forever.

What is a Structured Settlement?

A Structured Settlement is a financial arrangement where you receive your money in regular installments over a period of time.

Instead of one big check, you might get:

-

$2,000 every month for 20 years.

-

A specific amount every year for life.

-

A small lump sum now, followed by monthly payments later.

This is usually set up by purchasing an annuity (a financial product sold by insurance companies) that guarantees these payments.

Why Choose a Structured Settlement?

The biggest advantage is security.

-

Guaranteed Income: You know exactly how much money is coming in every month, just like a paycheck.

-

Tax Benefits: In many cases, the interest earned on these payments is tax-free (we’ll explain this more later!).

-

Spendthrift Protection: It prevents you (or greedy relatives) from spending all the money at once.

The Downside of Structured Settlements

The main drawback is inflexibility. Once you sign the papers, it is very difficult to change. If you have a sudden emergency—like needing $50,000 for a surgery—you cannot simply "withdraw" it from your future payments.

Comparative Advantage: The Tale of the Tape

To make this easier to understand, let’s look at a Comparative Advantage table. This method compares two options to see which one performs better in specific categories.

| Feature |

Lump Sum Payout |

Structured Settlement |

| Access to Cash |

High: You get 100% of the money immediately. |

Low: Money is drip-fed over years. |

| Financial Control |

High: You decide where every penny goes. |

Low: The insurance company controls the schedule. |

| Risk of Overspending |

High: Easy to blow the money on impulse buys. |

Low: You can only spend what you receive that month. |

| Inflation Protection |

Variable: Depends on how well you invest it. |

Adjustable: You can negotiate for payments to increase over time. |

| Tax Impact |

Medium: Investment earnings are usually taxed. |

Excellent: Growth and interest are often tax-free. |

| Best For |

Paying off immediate large debts (House, etc.). |

Long-term living expenses and medical care. |

The "Financial Expert" Perspective: Taxes and Growth

This is the part where 10th-grade math comes in handy. It’s not just about the total number; it’s about what you keep.

The Tax Trap

In the United States, proceeds from a personal injury settlement for physical injuries are generally tax-free.

-

If you take a Lump Sum: The $500,000 is tax-free. However, if you put that money in a bank or stock market and it earns $50,000 in interest, you must pay taxes on that $50,000 earnings.

-

If you take a Structured Settlement: The money grows inside the annuity. When you receive the payments years later, that "growth" is often still tax-free.

This "tax-free growth" is a massive comparative advantage for structured settlements. Over 20 or 30 years, this can equal tens of thousands of dollars in extra money that you wouldn't get with a lump sum investment.

Which Option Should You Choose?

There is no "one size fits all" answer. Here are a few scenarios to help you decide.

Scenario A: The Young Investor

Profile: You are 25 years old, have a minor injury that has healed, and you have a good job.

Verdict: Lump Sum.

Since you have a salary to live on, you can take the lump sum and invest it in a high-growth retirement account or buy a home. You have time on your side to ride out the ups and downs of the market.

Scenario B: The Long-Term Care Need

Profile: You suffered a severe injury that prevents you from working, and you need ongoing medical therapy.

Verdict: Structured Settlement.

You cannot afford to risk your money in the stock market. You need a guarantee that your rent and medical bills will be paid every month for the rest of your life. A structured settlement acts like the salary you can no longer earn.

Scenario C: The "Bad with Money" Victim

Profile: You admit that money "burns a hole in your pocket."

Verdict: Structured Settlement.

If you take a lump sum, you might buy a luxury car and go on vacations, leaving you with nothing for your future medical needs. The structured settlement protects you from yourself.

10 Expert Attorneys to Guide You

Making this choice involves complex legal contracts. You need an attorney who understands not just the law, but the financial implications of your settlement.

We have selected 10 expert attorneys featured on Best Attorney USA who deal with litigation, employment, corporate law, and complex financial matters. These professionals understand the high stakes of legal payouts.

-

Michael E. Hollingsworth II – Atlanta, GA

-

Christopher Avallone – Milwaukee, WI

-

Douglas J. Evertz – Costa Mesa, CA

-

Mark D. Pollack – Chicago, IL

-

Adam Augustine Carter – Washington, DC

-

John T. "Tom" Johnson, Jr. – Knoxville, TN

-

Joseph F. "Joe" Quinn – Pittsburgh, PA

-

Eric B. Levine – New Providence, NJ

-

Jay A. Dorsch – Philadelphia, PA

-

Adam V. Maiocco – Shelton, CT

You can find more information about these attorneys and search for local representation directly at BestAttorneyUS.com.

Conclusion

The choice between a Structured Settlement and a Lump Sum Payout isn't just about math; it's about your life.

If you value security, tax-free growth, and discipline, the structured settlement is your best friend. It ensures you will never be penniless because of a bad investment or a spending spree.

If you value flexibility, control, and immediate debt relief, the lump sum might be the better path—but only if you have a solid plan and the discipline to stick to it.

Before signing any settlement agreement, you must consult with a qualified attorney and a financial planner. They can look at your specific debts, your age, and your medical needs to build a plan that lasts.